Market sentiment report

Labour shortages and major increases in the cost of construction materials are seeing the construction sector across the nation overheat.

Labour shortages and major increases in the cost of construction materials are seeing the construction sector across the nation overheat.

The latest construction industry market sentiment report, released by Arcadis and the Australian Constructors Association in May 2023, reveals that the recent inflationary crisis continues to have a severe and far-reaching impact on Australia’s construction industry.

All surveyed contractors reported having to absorb material price escalation in 2022 that could not be recovered or offset in any way. Despite some improvement since the last survey, a significant 76% of respondents believe that the current commercial environment still unfairly and unreasonably allocates risk between clients and contractors.

Risk allocation has been identified as the most significant barrier to innovation and productivity growth in the industry and, to put this into perspective, the industry’s productivity performance is at a 30-year low.

While the report indicates material price inflation is beginning to moderate, the cost of labour is starting to increase significantly. More than half of respondents rated trade labour capacity as severely constrained compared to only 20 per cent last year.

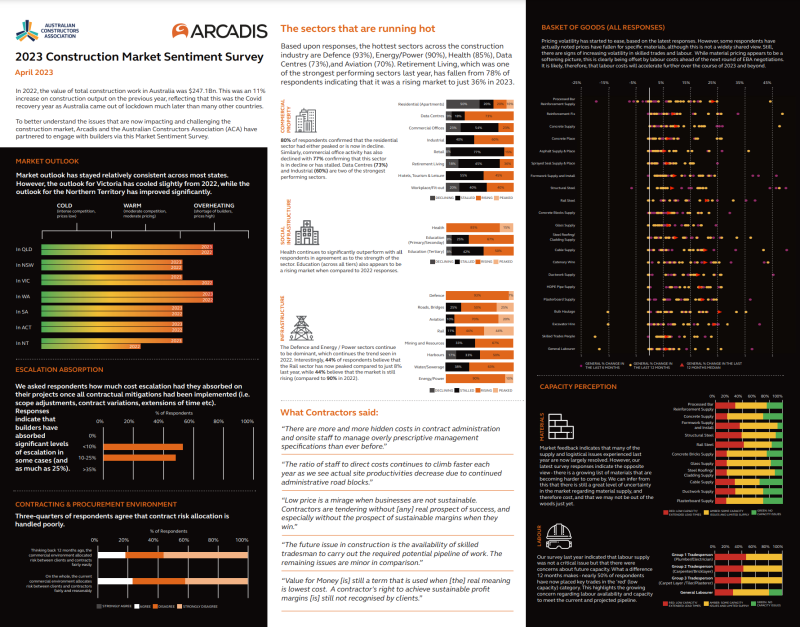

The industry expects that market will remain overheated in 2023, with a shortage of contractors relative to demand, and prices remaining high. “Based upon the responses received, Queensland and Western Australia are anticipated to be the hottest markets, while overall sentiment has fallen in Victoria compared to last years survey.

In terms of asset classes, Defence, Energy and Power, Health, Data Centres and Aviation are the strongest performers. Interestingly, enthusiasm for the Retirement Living sector has fallen since last year – with just 36% of respondents indicating that this is a rising market compared to 78% in 2022.

The latest data also indicates that pricing volatility for materials has started to ease, which some respondents noting that prices have fallen for specific items. While material pricing appears to be a softening picture, this is now being offset by increasing labour costs ahead of the next round of EBA negotiations. We therefore anticipate that labour costs will become a primary driver of the next wave of construction cost inflation.

Key statistics

Further information: